Read the latest WaveData articles, or search through our archive.

Follow us on LinkedIn to keep up to date with WaveData news, articles, insights and analysis

Please use complete words when searching…

WaveData Case Study – Bespoke Reports: Generics Market Assessment

Client X is launching a new generic product into the UK market, they were looking for data to assess market potential, support their forecasting and feed into the commercial strategy.

Our Customer Success Manager and Data Team worked closely with the Client’s Portfolio Manager and Commercial Manager to ensure we provided the right data for their project needs.

WaveData investigates the ongoing shortage of Naftidrofuryl Caps 100mg 84

Since Jan 2021 Naftidrofuryl Caps 100mg 84 has been granted concessions in 25 out of 29 months…….

WaveData Analysis | Long Term Pricing Trends | Aripiprazole Tabs 5mg 28

This product was launched in December 2014 and has had a reasonably stable price there after. The average price came down very quickly, reaching stability by mid 2016. However, since then this product has experienced a couple of price bounces where the average price rose unexpectedly, concessions had to be granted and increases in the drug tariff followed. Monitoring the price and setting a low watch point could help us identify a future bounce.

How serious is the issue of shortages in the UK Pharma market asks Charles Joynson?

There are two primary ways in which shortages are flagged for pharmacists and dispensers. The first is the granting of a concession for generic products and the second is the product’s addition to the NHS’ serious shortage protocols (SSP) list. These have both been operating for some years and the number of products in each has been growing. The number of generic concessions granted each month has risen to nearly 200 whilst the number of SSPs is approaching 20.

This is the situation at present….. However, there is a threat that shortages might get much worse. This is driven by the voluntary scheme for branded medicines pricing and access (VPAS) and by the rebates paid back by manufacturers of branded and branded generic drugs as part of this scheme. Previous analyses by Wavedata have suggested that 22% of branded medicines and 49% of branded generics do not have sufficient profitability to survive the high rebates and are likely to be removed from sale in the UK.

Ten Years of Generic Galenical (Liquid) Market Prices

The liquid forms of common medicines are often forgotten about when the focus is on their big sister the solid dose forms. However, liquid forms of common generics have been shown

to maintain high prices for long periods because there is less competition between manufacturers for these more niche products.

Will the Windsor Framework stop the decline of available medicines in Northern Ireland?

One of the main objectives of the Windsor Framework is to provide a permanent solution to safeguarding the supply and access of medicines into Northern Ireland. We can see from our historical data that there has been a steady decline of the number of products that are available in Northern Ireland, will the trend be reversed once the new Green Lane is open?

DHSC SSP announcements hitting Paracetamol 240g Suppositories

With last week’s DHSC SSP announcements hitting Paracetamol 240g Suppositories, we’ve taken a look at long term pricing trends, and the most recent data in our Live system.

Antibiotic prices soar and availability plummets

The prices pharmacists and dispensing doctors pay for antibiotics have risen in recent months amidst shortages and concessions. The product which rose the most between Jan 2022 and Jan 2023 was Co-Amoxiclav Tabs 500mg/125mg 21 which rose from an average price of £1.39 in Jan 2022 to £8.50 in Jan 2023, an increase of 512%.

Is the VPAS Scheme doing more harm than good? Part Two…….

VPAS continues to be one of the top priorities for the UK Pharma Industry. A week or so ago, we undertook some analysis on Originator Brands, assessing profitability and UK market attractiveness. If the rebate is unsustainable, and results in loss making products for manufacturers, we could see withdrawal from the market, driving supply challenges and increases in market pricing.

Is the VPAS Scheme doing more harm than good?

Although the aim of the VPAS scheme is to support innovation and better patient outcomes, alongside keeping a lid on the NHS drug budget, could the scheme actually be doing the opposite? If the rebate is unsustainable, and results in loss making products for manufacturers, we could see withdrawal from the market, driving supply challenges and increases in market pricing.

Statins prescribing to reduce the risk of cardiovascular events

We’ve all read the latest from NICE on the revised recommendations for the use of Statins to reduce the risk of cardiovascular events. It’s been widely shared that there are currently 10 million eligible patients in the UK, and this could rise to as many as 25 million with the new advice. WaveData’s ScriptMap service tells us that a little over 95 million prescriptions were issued for Statins in the last full year of available data, so we could be looking at almost 240 million prescriptions under the new guidelines.

The Largest Antibiotic Price Rises Jan to Dec 2022

With the recent increase in bacterial infections and the shortage of Strep A antibiotic drugs such as penicillin and amoxicillin, Wavedata thought it worth looking at all the antibiotics used in the community in the UK to see which have experienced the greatest price rises.

Atorvastatin Tabs 20mg 28, Profit and Loss.

Atorvastatin Tabs 20mg 28 was launched in the UK in May 2012 and since then the price has declined gradually. However, there have been some price rises along the way which have been very noticeable. The first of these happened in 2013, the second in 2020 and the third may be happening now.

Procoralan-Ivabradine Parallel Import and Generic Market Activity Since Launch

Branded Procoralan first appeared on price lists sent to pharmacists and dispensing doctors in the UK in February 2008, followed 5 months later in July 2008 by parallel imported versions.

Ezetrol-Ezetimibe Parallel Import and Generic Market Activity Since Launch

Branded Ezetrol first appeared on price lists sent to pharmacists and dispensing doctors in the UK in June 2004, accompanied in the same month by the first evidence of parallel imports.

Cialis-Tadalafil Parallel Import and Generic Market Activity Since Launch

Branded Cialis was launched in the UK March 2003, which was followed in July 2004, 16 months later, by the appearance of the first parallel import. The number of monthly offers for the PI peaked in October 2008 at 137 market offers in a single month.

Crestor-Rosuvastatin Parallel Import and Generic Market Activity Since Launch

Branded Crestor was launched in the UK June 2003, and this was followed by the appearance of the first parallel import just one month later. The number of market offers in price lists for parallel imported versions of Crestor follows a typical ‘whale’s back’, with a rapid introduction in 2004 and 2005, an erratic build up to a peak in 2011, and a gradual decline toward 2022.

Amoxicillin Market Price Increases

Infections with the Group A Streptococcus (GAS ) are very common at the moment and can cause Scarlet Fever. This mainly affects children and Amoxicillin is the most common treatment. However, the availability of and prices of Amoxicillin products for pharmacies and dispensing doctors has been put under pressure by this outbreak.

Total concessions (NCSO) granted each month. Will they become permanent?

Since price concessions were first granted in 2003, the number has been gradually increasing each month. During 2022 the number granted has equalled or exceeded 100 in 8 months out of 11. Additionally we have noticed that products likely to be granted concessions have very narrow pharmacy profit margins. This makes sense since it is the PSNC, representing pharmacies, which negotiates concession with the department of health DHSC. However, this increasing trend highlights a serious problem with the way these products are reimbursed. This is done using the drug tariff, and in order to supply good value for tax payers some products have their tariff squeezed as much as possible. This may be great for tax payers in the short term, but it’s not great for pharmacies, wholesalers and manufacturers. Pharmacies struggle to make a profit, despite the concession, as often it’s not high enough and they spend inordinate amounts of time chasing shortages.

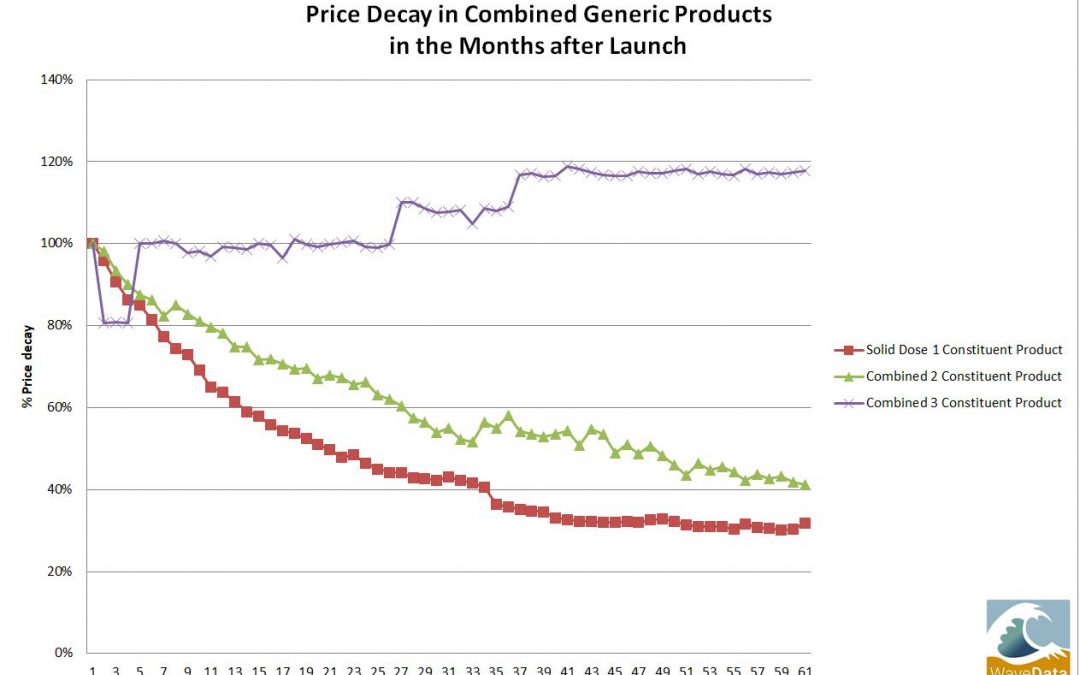

Price Decay in Combined Generic Products in the Months after Launch

Do combined, multi constituent products which contain more than one chemical, such as Levodopa + Carbidopa + Entacapone Tabs, suffer slower price decay after generic launch than normal single constituent products? It would make sense to assume so as we have previously found that products such as liquids, devices , creams and ointments all decay more slowly than solid dose generic products.

Follow us: