Read the latest WaveData articles, or search through our archive.

Follow us on LinkedIn to keep up to date with WaveData news, articles, insights and analysis

Please use complete words when searching…

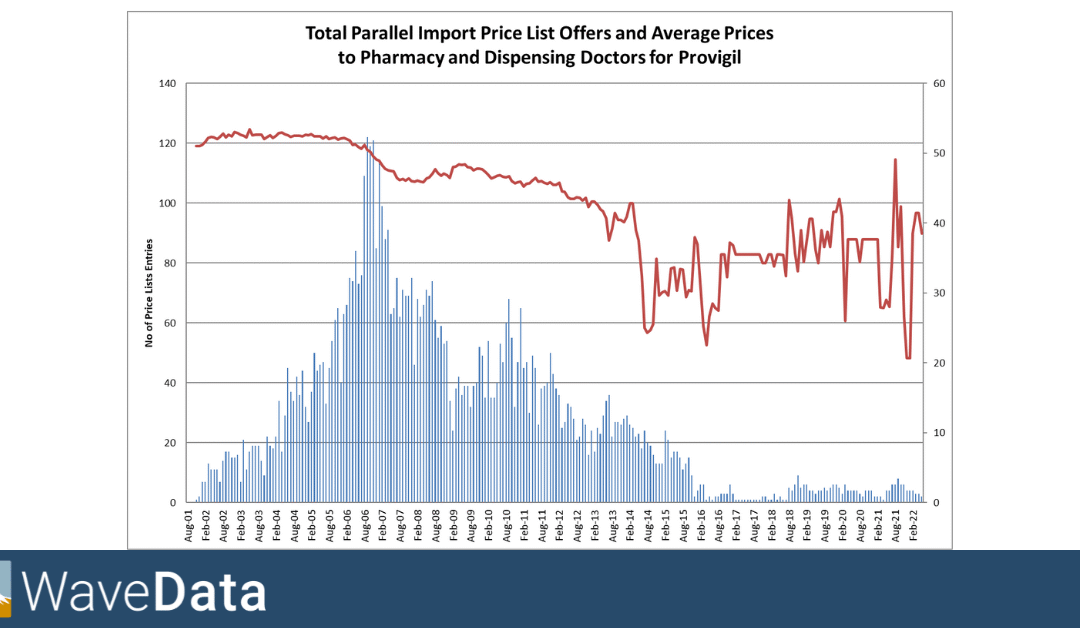

The Life and Death of Imported Provigil

Provigil was launchd in the UK in March 1998 and it is used to promote wakefulness in patients with narcolepsy, a condition characterized by excessive daytime sleepiness. The first sign of parallel imports being sold into the UK was in November 2001, and though a trickle at first it grew to a peak of over 120 price list inclusions each month by September 2006, which meant that pharmacists and dispensing doctors had lots of opportunity to buy the imported version of the UK brand.

Changes in the number of drug tariff products

Between 2001 and 2022 the number of generics in the English drug tariff increased from 1682 to 3955. Most of this was driven by increased patient demand and new product launches to cope with this demand.

The Life and Death of a Parallel Import

The WaveData Team wanted to find an example of a parallel import appearing in the UK, it’s birth in competition with the UK brand, and it’s final demise once generics had hit the market.

We looked at all the different constituent molecules for which we had been able to collect parallel import information over the last 25 years. There were quite a large group of these, but we chose one that had very high numbers of market offers on price lists to dispensing doctors and pharmacies roughly in the middle of the 25 year period.

Drug or Device? Have devices increased their presence in the last 25 years?

Each month WaveData collects the prices of medicines and devices from pharmacies and dispensing doctors. These come from the price lists and invoices sent to these accounts by their suppliers. So what we’re looking at here is the ‘share of voice’ rather than market share, which specifically means the amount of effort put into advertising these products to accounts.

Brands and Generics. How has their ‘share of voice’ changed in 25 years?

Each month WaveData collect the prices of brands and generics from pharmacies and dispensing doctors. These come from the price lists and invoices sent to these accounts by their suppliers. This means that what we’re looking at here is the ‘share of voice’ rather than market share, which specifically means the amount of effort put into advertising these products to accounts.

Generics Bulletin Price Watch

Check out the latest UK Price Watch article in the Generics Bulletin for analysis and insight on May’s product launches, the biggest risers, the biggest fallers and the fastest movers…. with market data provided by WaveData.

Sitagliptin Long Term Price Analysis – After the Fall, Loss of Exclusivity and Generic Entry

Before December 2022 when generics were launched, all prescriptions, branded and generic would have been dispensed as MSD’s Januvia Tabs 100mg 28. This explains why the generic and branded lines on the graph follow the same trend. The green PI average price line does follow the other two, but prices do seem to have been slightly higher over the seven years leading up to loss of exclusivity. Pharmacists often assume that parallel imports are cheaper than UK packs, which is not always the case.

The Terrible Twos

Pramipexole Tabs 88mcg 30 is one of those products that suffers regular price bounces. In this case it seems to be almost exactly every two years, which in our minds fits with manufacturing cycles.

Long time survival in the commercial pharma bear pit

Prior to the launch of generics in August 2011 the UK and Parallel Imported (PI) packs of Keppra Tabs 250mg 28 had very similar prices. However, post August 2011 the market changed completely. Firstly, generics appeared in the market and took six months to fall from £25 down to £5, secondly the UK brand price dropped considerably from around £29 to closer to £22, and finally the PI price started to decline and has continued to drop ever since.

Is DHSC Trying to Break Pharmacy?

We know that when a product’s market price is above the Drug Tariff, it tends to mean that there’s a shortage, and competitive buying and selling has increased market prices. We decided to count the number of products each month where the market price was higher than the Drug Tariff. We did not count products where the market price and the Drug Tariff were the same, and we did not include products that were not in the Drug Tariff.

How Profitable is Dispensing?

Recently Charles Joynson, WaveData MD, ran a pricing analysis on Acetazolamide Tabs 250mg 112 and found that Pharmacies and Dispensing Doctors had been losing £18.00 each time they dispensed this product in the three months to end March. Today we thought we’d look at all the generic products in the drug tariff to see how many are profitable and how many are unprofitable.

Acetazolamide and the Pharmacy Killer

Acetazolamide is a product which has suffered major shortages worldwide over the last few years. The average market price of the 250mg 112 tablet pack fell from over £75 ten years ago, to a low of £15.43 in May 2020, and then rose to a peak of £24.18 in November 2024.

Charles Joynson, WaveData MD looks at the ‘Covid Effect’ on prices of Non-Steroid Anti Inflamatory Drugs.

When people caught Covid in the early months of 2020, they normally reached for symptomatic control using NSAIDs and Paracetamol. They are affordable, widely available over the counter, have a well-established benefit-risk profile and are good at managing fever, body aches, and headache.

At the time there was pressure on supply, but looking back what happened to prices?

Charles Joynson, WaveData MD, analyses Naproxen E/C Tabs long-term pricing.

The curious wave form or cyclicity of the prices of these two products demonstrate the vulnerability the supply chain has to unprofitable low prices. In the period between 2000 and 2007 both products drifted along with low market prices. For the 250 mg pack this meant prices were generally below £3.00 and for the 500 mg prices were below £5.00.

WaveData MD, Charles Joynson, investigates Tadalafil Tabs 2.5mg 28 Long Term Pricing Trends

Tadalafil Tabs were launched in November 2017 in competition with Eli Lilly’s Cialis Tabs. Generic prices post launch were around the £10.00 mark, significantly lower than the Cialis reimbursement price at the time which was £54.99. However, eight months after launch in July 2018 the main generic manufacturer increased its prices from £5.50 to £45.00 per pack.

Charles Joynson, WaveData MD, investigates Quetiapine Tabs 100mg 60 Long Term Price Trends

Over the last ten years Quetiapine Tabs 100mg 60 has had 4 sets of concessions, making it a risky product to make and distribute. WaveData wanted to find the ‘trigger’ prices which forced manufacturers out of the market due to unprofitability.

WaveData MD, Charles Joynson takes a closer look at Clarithromycin Suspension 250mg/5ml 70ml Concessions and Shortages.

This suspension is one that has been hovering on the edge of unprofitability for a long time and has seen more concessions granted (32) in 2023 – 2024 that any other generic.

Travoprost + Timolol Eye Drops 40mcg/5mg/ml 2.5ml Long Term Price Trends

This product has seen its market price decay from around £13.00 in 2017 – 2020 to a low of £4.29 in September 2024. This may have pushed this combined product, complicated to make due to its combined and device characteristics, into unprofitability as it has been granted concessions in 2022, 2023 and 2024.

Is the number of concessions granted each month increasing or declining?

With the number of concessions granted by DHSC in October at just 106, the lowest number since May 2022, we wondered if this was a signal of a reduction in the number of shortages or if it was just a blip?

Huge price spikes of Apixiban 5mg 56 drive investigation of the long term view of both the generic and brand.

WaveData’s Head of Data, Natalie Fancourt, alerted us to the huge price spikes on Apixaban 5mg 56. Charles Joynson, WaveData MD, decided to investigate the longer term view of both the Generic and Brand.

Follow us: